Caring for a person in need can be exhausting and frustrating. Having to make decisions for another person’s health is almost a full-time job. I know. I did it for my mom for three years. During that time, I’ve learned things that can help you avoid mistakes I made. So, here are some answers to commonly asked questions.

First let me start by saying, those of you who are in this role, you are angels without wings. As you age, you will see how important the assistance you provided was and the huge difference it made in savings, comfort, peace of mind and, of course, quality of life. So, when you feel like throwing in the towel, take a deep breadth and know you are storing treasure in Heaven and making a difference.

This will be a four-part series covering 16 questions regarding care for seniors and the disabled, whether veteran or civilian. We will talk about:

- SSD and SSI recipients

- Veterans benefits and Tricare for Life and VA Champs

- Medicare beneficiaries

- What to do if you have an overdose due to dementia.

- What resources are available for those who need care while the caregiver is working.

- Coverage while traveling

- And more!

So, if you have not subscribed to our newsletter, you may want to do so to avoid missing these must-read articles. Okay, let’s get to the first four questions.

How can I learn what my care receiver is eligible for?

There are several ways you can check eligibility:

- Online at SSA.gov (if you don’t have an account, create one)

- Calling Social Security directly at 800-772-1213 (for TTY call 800-325-0778)

- Calling Medicare at 800-Medicare (800-633-4227)

- Calling a licensed insurance agent who specializes in Medicare

The easiest and most beneficial is the last one. By calling a fiduciary, like YourCareRep.com, you have an agent who does not work for any insurance carrier; however, he or she contracts with multiple to be able to find the best fit for your needs. We can call very easily and learn what your care receiver is eligible for and provide guidance on other programs (if he or she qualifies) that they may qualify for.

Medicare and Social Security are behemoth organizations who are not designed for individual assessment. While an agent specializes in your area and having helped hundreds of people, know the intricate details of the system and how they best help you.

Drug copays are too expensive. Is there any help available to lower prescription costs?

If your care receiver is on Medicare, then he or she may qualify for the Extra Help (LIS) program. LIS stands for low-income subsidy. There are certain criteria that must be met. They include:

- How many people live in your household? For example, if your grandchildren live with you, or your care giver lives with you, then they are added to the number of the household.

- How much do you earn, annually?

- Other than your home, car and any term life insurance you may have (these are not counted as assets or resources), how much do you have in assets and resources?

If you click here, then click on See 2021 Federal Poverty Levels, you can see the qualifications. If you do qualify or believe you may, you can go apply for Extra Help here.

Even though my care receiver has insurance, he or she still can’t afford the bills. What are his or her options?

If you are having difficulty sustaining yourself financially, you can also apply for a Medicare Savings Program (MSP – Medicaid assistance). When you looked at the 2021 Federal Poverty Levels to see if you qualify for Extra Help, if you fall into the 135% or less column, then you may also qualify for an MSP.

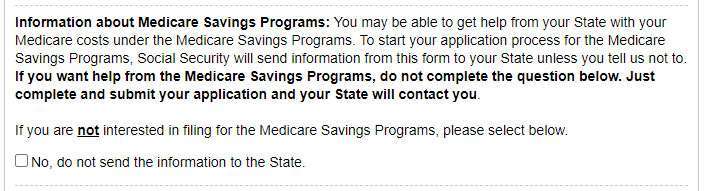

When filling out the application for Extra Help, you will see the following question:

If you wish to apply, DO NOT CHECK THE BOX! If you check the box, they will not send your information to the state to apply for an MSP.

With so many plans to choose from, how do I know I’ve chosen the right plan for my care receiver?

This is a very good question. While you can figure this out on your own, it would be easiest to speak with a fiduciary agent. They will conduct a needs analysis to identify what your care receiver may be eligible for and make suggestions based on:

- Financial resources

- Lifestyle

- Health conditions (if necessary to choose a Special Needs Plan)

- Goals

- Providers and facilities available

- Benefits and incentives

When choosing a plan, all the above must be considered. If your care receiver qualifies for the aforementioned programs (Extra Help and MSP), they will help you enroll. If they don’t, there may be plans that provide Part-B premium givebacks that help pay the premium Medicare deducts from his or her social-security check.

If your care receiver is a frequent traveler, certain plans need to be considered that may provide a broader network that can be used while traveling, and/or emergency and urgent care while on the road. While many plans offer the latter, not all benefits are equal. You will want to look at the Summary of Benefits to determine which one is right for your care receiver.

Also, many plans offer different forms of additional benefits and incentives that add up to real money in one’s bank account. Such as:

- Over-the-counter allowance (OTC) of $20 to $100 per month for items you are currently buying at CVS, Walgreens, Walmart or your favorite store.

- Food cards ranging from $25 to $100 per month for grocery items.

- Dental benefits that are either insurance or an allowance.

- Free transportation to appointments which saves on gas or Uber.

- Free meals after hospitalization.

- And more, depending on the plan.

If you feel you may have the wrong plan, you can change it during an election or enrollment period. There are four kinds of election periods:

- (IEP) Initial Election Period (when you are turning 65)

- (AEP) Annual Election Period (October 15th through December 7th)

- (OEP) Open Enrollment Period (January 1st through March 31st – only for Medicare Advantage beneficiaries)

- (SEP) Special Election Period.

SEPs are triggered when special circumstances occur. There are quite a few. While this list is not extensive, it gives you an idea of when you may be able to change a plan, should the need arise.

- If your financial situation changes for the worse.

- If you move out of your plan area.

- If your plan were to be cancelled or you are disenrolled (like when moving).

- If your health condition changes.

If you feel you need to change your plan and do not know if you are eligible to do so, always remember you can engage an agent who will help you. We have access to resources that allow us to get you answers quickly, instead of being on endless hold with Medicare or Social Security.

Next week’s article will answer the following questions:

- What’s the difference between SSD/SSDI and SSI, and why it matters?

- How does SSD/SSDI and SSI affect when one qualifies for healthcare benefits?

- My care receiver, who’s on SSD/SSDI is eligible for Medicare. What should I do?

- My care receiver didn’t take Medicare Part-B because he or she couldn’t afford the premium. What are his or her options?

Again, if you found this article on Facebook or LinkedIn and found it helpful, subscribe to our newsletter so you don’t miss the next three (3) articles in the series. Furthermore, if you have a particular question, feel free to email it to ed***@*********ep.com, or post it in the comments section below. I will get back to you rapidly with an answer. Stay tuned!